Last year’s Hurricane Helene wasn’t just a coastal disaster – it became a historic inland catastrophe. The unexpected devastation it caused in the mountains of North Carolina stunned forecasters and insurers alike. As the 2025 hurricane season unfolds, the lesson is clear: insurers can’t afford to be caught off guard again.

The 2025 Atlantic hurricane season officially began on June 1 and runs through November 30. Early forecasts suggested an above-average season, with elevated risks for several U.S. regions. For insurance professionals, carriers, and risk managers, understanding these projections is crucial to anticipating the 2025 hurricane season insurance impact on portfolios and claims.

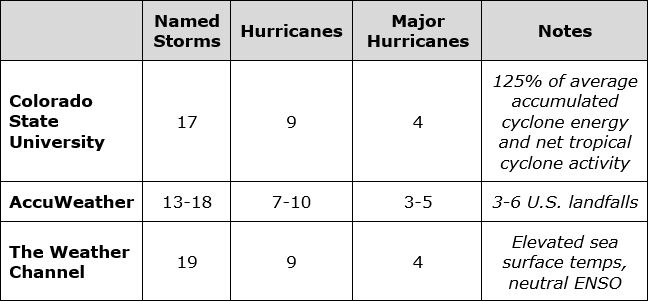

2025 Hurricane Season: Early Forecasts

The official NOAA outlook – typically released in late May – provides the most up-to-date assessment of potential storm activity. For insurers and risk managers, tracking both preliminary forecasts and the latest updates ensures a well-informed approach as storm activity intensifies through the summer and fall.

- Colorado State University: In early April, CSU, which pioneered seasonal hurricane forecasting in 1984 (well over a decade before NOAA began its forecasts), predicted 17 named storms, 9 hurricanes, and 4 major hurricanes (Category 3 or higher) for the 2025 season. These numbers represent increases of approximately 18%, 25%, and 25%, respectively, over the 1991-2020 averages. Additionally, the forecast anticipates accumulated cyclone energy and net tropical cyclone activity to be about 125% of their long-term averages – indicating a potentially more intense and prolonged hurricane season.

- AccuWeather: Its early forecast predicts 13-18 named storms, including 7-10 hurricanes and 3–5 major hurricanes. Notably, AccuWeather predicts 3-6 storms could make direct U.S. landfalls. The forecast emphasizes the potential for rapid intensification of storms, driven by extreme sea surface temperatures, which could lead to heightened risks for coastal regions.

- The Weather Channel (The Weather Company): Partnering with Atmospheric G2, The Weather Channel anticipates an above-average 2025 Atlantic hurricane season, projecting 19 named storms, 9 hurricanes, and 4 major hurricanes. Their forecast highlights warmer-than-average sea surface temperatures and a neutral ENSO pattern as key factors contributing to increased storm activity and a higher likelihood of U.S. landfalls.

These early forecasts underscore the potential for a significant 2025 hurricane season insurance impact, with insurers advised to monitor conditions closely. The projections are influenced by several key climate factors – namely, sea surface temperatures and El Niño vs. La Niña conditions.

Sea Surface Temperatures

Warmer ocean waters act as high-octane fuel for hurricanes. When sea surface temperatures rise above average, particularly in the main development region between West Africa and the Caribbean, it creates ideal conditions for storms to form and rapidly intensify. Current readings show Atlantic waters are already significantly warmer than normal, increasing the likelihood of stronger and longer-lasting storms. This contributes directly to the expected 2025 hurricane season insurance impact, as stronger storms often result in larger, more complex claims.

El Niño vs. La Niña

The climate pattern known as El Nino-Southern Oscillation (ENSO) plays a critical role in hurricane activity. During La Niña, reduced wind shear over the Atlantic often leads to more storms, while El Niño typically suppresses hurricane formation. This year, the Pacific has already transitioned to ENSO-neutral conditions (when neither El Niño nor La Niña is dominant), reducing forecasting certainty but still supporting an active hurricane season when combined with unusually warm Atlantic waters.

In recent years, tropical storms have increasingly formed before the official start of hurricane season – a trend challenging long-standing assumptions about when and where these systems develop. For insurers, this unpredictability reinforces the importance of early preparedness and continuous monitoring to protect portfolios against escalating loss potential throughout the season.

Geographic Risk Assessment: Expanding Vulnerabilities Across the U.S.

While Florida often captures the spotlight during hurricane season, the 2025 forecasts highlight a growing reality:

No coastal region is immune – and even inland areas are increasingly at risk.

The Gulf Coast, Southeast Atlantic, and Northeast all face elevated threats this year, a concern amplified by the unprecedented reach of last year’s Hurricane Helene.

Florida & the Gulf Coast: Persistent High Risk

Florida’s extensive coastline and low-lying terrain keep it at the forefront of hurricane exposure. In 2025, forecasts again signal elevated risks, particularly along the Panhandle and western coast. The Gulf Coast – spanning Texas to Alabama – is also bracing for what could be a highly active season. According to Colorado State University’s April forecast, there’s a 70% chance of a named storm passing within 50 miles of the Texas coast, well above the historical average. With these elevated probabilities, insurers along the Gulf Coast face a heightened 2025 hurricane season insurance impact.

The impacts of Tropical Storm Beryl and Hurricane Helene remain top of mind for many communities, serving as recent reminders of how quickly storms can escalate and disrupt regions far beyond their projected paths.

Southeast Atlantic Coast: Emerging Hotspot

The destructive path of Hurricane Helene didn’t end in Florida. After crossing the state, it continued to batter coastal Georgia and the Carolinas – regions without a direct hit in over a decade. Urban centers like Charleston, Savannah, and Wilmington were caught off guard by the storm’s rapid intensification and unpredictable trajectory.

This alarming case has prompted meteorologists to issue warnings about climate factors – such as warmer ocean waters and shifting atmospheric patterns – making storms more likely to veer off traditional paths and impact areas previously considered lower risk. For insurers and reinsurers, this greatly complicates geographic risk models, which have historically relied on more predictable patterns of storm behavior. Insurers operating in these regions should prepare for the 2025 hurricane season insurance impact to stretch beyond historical loss patterns.

Northeast U.S.: A False Sense of Security

Though less frequent, storms reaching the Northeast are often underestimated – a complacency proven costly in recent years. Hurricanes like Isaias (2020) and Ida (2021) brought widespread flooding, wind damage, and prolonged power outages to states including New Jersey, New York, and parts of New England. Ida, in particular, caused historic inland flooding across the New York City metro area and served as a stark reminder: A storm’s most destructive impacts aren’t limited to where it makes landfall. Even regions viewed as low hurricane risk remain vulnerable to catastrophic outcomes, especially when powerful storms stall over urban centers with aging infrastructure and poor flood resilience.

Implications for the Insurance Industry: Navigating a Complex Landscape

In 2024, hurricane-related losses for Helene and Milton alone impacted 6 states and exceeded $100 billion in damage. This underscores the urgent need for insurers to reassess their risk portfolios before peak season arrives.

Hurricane Helene demonstrated how storm unpredictability – and the growing number of high-cost claims it can trigger – demands sharper forecasting, faster response times, and smarter risk modeling. An above-average hurricane season presents multifaceted challenges for the insurance industry, affecting everything from underwriting to claims management.

1. Underwriting & Risk Assessment

Insurers must reassess their risk models to account for the increased likelihood of severe weather events. This includes evaluating the potential for rapid intensification of storms, a phenomenon where hurricanes strengthen quickly before landfall, leaving little time for preparation. Such events can lead to higher-than-expected losses, challenging traditional underwriting assumptions. These underwriting challenges are central to managing the 2025 hurricane season insurance impact effectively.

2. Claims Management & Operational Readiness

The uptick in storm activity necessitates enhanced claims management strategies. Insurers should invest in scalable claims processing systems and train adjusters for rapid deployment to affected areas. The goal is to expedite claims settlements, thereby aiding in swift community recovery and maintaining customer trust.

3. Reinsurance & Capital Allocation

The anticipated increase in hurricane activity may tighten reinsurance capacity and drive higher costs, making it critical for insurers to evaluate reinsurance treaties and explore alternative risk transfer mechanisms, such as catastrophe bonds, to ensure adequate coverage. Strategic capital allocation will be crucial to absorb potential losses and maintain solvency.

Following the 2024 season, U.S. property catastrophe reinsurance rates declined by approximately 6.2% during the January 2025 renewals. However, insurers with significant losses from events like Hurricanes Helene and Milton experienced stable or increased reinsurance costs, a trend likely to persist if high-loss events continue in 2025.

4. Regulatory Compliance & Reporting

Regulatory bodies may impose stricter reporting requirements and solvency standards in response to heightened risks. Insurers must stay abreast of evolving regulations and ensure compliance to avoid penalties and maintain their licenses. These regulatory shifts are a critical consideration when evaluating the broader 2025 hurricane season insurance impact.

5. Customer Communication & Education

Proactive communication with policyholders about coverage options, deductibles, and claims processes is essential. Educating customers on mitigation measures, such as installing storm shutters or reinforcing roofs, can reduce potential losses and enhance customer satisfaction.

Navigating an Active Hurricane Season: What Insurance Leaders Need to Know

With the 2025 Atlantic hurricane season already in motion, the insurance industry must remain vigilant as storm activity peaks between August and October. For insurers and risk managers, the question isn’t whether this season will bring challenges – but whether their portfolios are prepared to withstand them. By staying informed and implementing proactive strategies, insurers can navigate the 2025 hurricane season insurance impact with greater confidence.

At Windward Risk Managers, we help carriers protect their portfolios with expert risk insights and forward-looking management strategies. To learn more about our services, email us at marketing@windwardrisk.com or call us at 888-514-4037. Or learn about the carriers we manage: Florida Peninsula Insurance Company, Edison Insurance Company, and Ovation Home Insurance Exchange.